Projects stalled

due to financing are beginning to resurface.

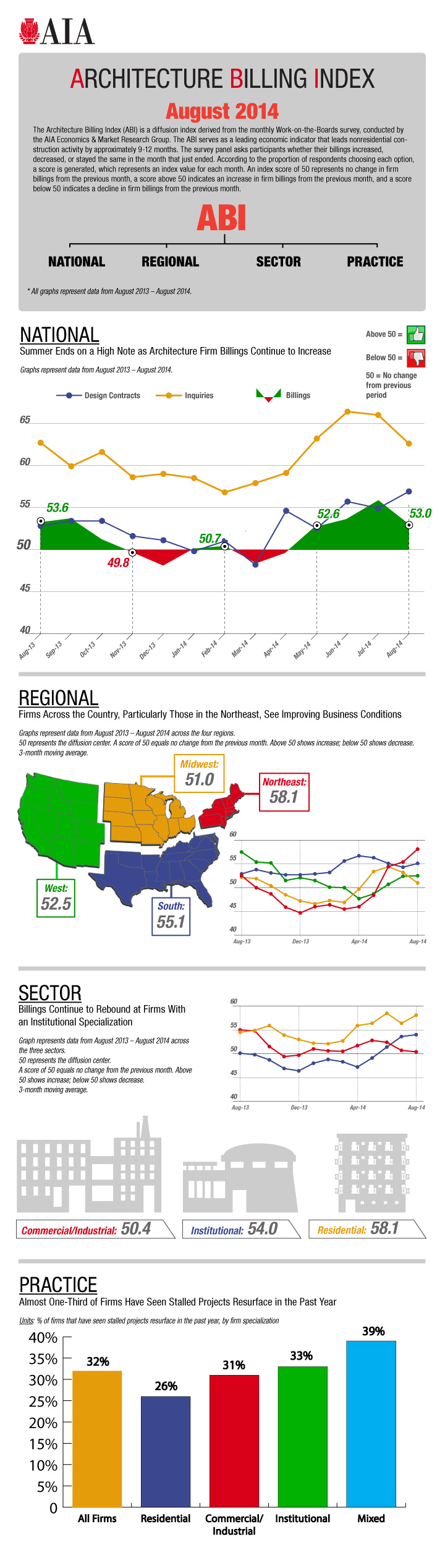

Business conditions continued to improve at architecture

firms in August, although the ABI score of 53.0 (any score over 50 denotes

billings growth) indicates that firm billings increased at a slightly slower

pace in August than in July. However, the outlook for the coming months remains

positive, as the value of signed design contracts, which indicates upcoming

work in the pipeline, continued to increase this month, and inquiries into new

projects remained strong as well.

For the third consecutive month, architecture firms in

all regions of the country experienced billings growth in August. The strongest

conditions were reported by firms in the Northeast region once again, coming on

the heels of a stretch of declining billings from October 2013 through May 2014.

Firms located in the South have seen the longest sustained period of billings

growth, now extending to more than two years.

Firms of all specializations also reported improving

business conditions for the third consecutive month. Conditions have been

positive for firms with a residential and commercial/industrial specialization

for all of 2014 so far, but firms with an institutional specialization spent

much of that time experiencing softening billings, and only recently have

started to recover from that brief setback.

Conditions in the general economy also softened somewhat

in August, with payrolls increasing by only 142,000 positions, down from an

average monthly increase of more than 200,000 over the previous year. However,

the combined architectural and engineering services sector was a bright spot,

adding 3,000 positions, while in July (the most recent data available) the

architectural services sector grew to 164,800 jobs, the highest it has been in

four and a half years.

The latest edition of the Federal Reserve Beige Book,

released the first week of September, also shows some more mixed conditions,

with just half of reporting districts across the country showing growth in

residential or nonresidential real estate activity. There was an increase in

multifamily construction in the Boston, New York, and Dallas districts, while

nonresidential activity was more mixed in the New York and St. Louis districts.

During the economic downturn, many architecture firms had

projects that were delayed or cancelled for a variety of reasons. More than

three-quarters of firms (76 percent) indicated in this month’s survey that they

had major design projects that were significantly delayed or cancelled for

economic/financing reasons. And just under one-third of firms (32 percent)

reported that they had projects stalled due to financing issues that have now

resurfaced in the last year as substantially the same projects as originally

conceived. Firms with a residential specialization were both less likely to

report that they had stalled projects due to financing reasons, and that these

projects have resurfaced, while firms with an institutional specialization were

slightly more likely to see their stalled projects resurface in the last year.

And architecture firms with stalled projects tended to

believe that these projects will continue through construction, with 34 percent

of firms believing that more than one quarter of their stalled projects will

proceed to construction, and 37 percent believing that at least 10 percent to

25 percent of these projects will proceed. Fewer than 30 percent of firms think

that less than 10 percent of stalled projects will proceed to construction.

This month, Work-on-the-Boards participants are saying:

This month, Work-on-the-Boards participants are saying:

• A lot of multifamily rental residential projects are

underway or being started.— 6-person firm in the Midwest, residential

specialization

• In Midwest construction markets, project budgets are

being challenged with significant increases in construction inflation due to

limited labor availability.—95-person firm in the Midwest, institutional

specialization

• Generally, Middle Tennessee seems to be booming again.

There is a lot of activity on the design and construction front and we believe

we will continue to grow our firm this year.—5-person firm in the South,

commercial/industrial specialization

• There are lots of larger projects moving forward, but

smaller commercial and government work is still stalled.—6-person firm in the

West, institutional specialization

Source: AIA

No comments:

Post a Comment